Keep up with the ever-evolving AI landscape

Unlock exclusive AI content by subscribing to our newsletter!!

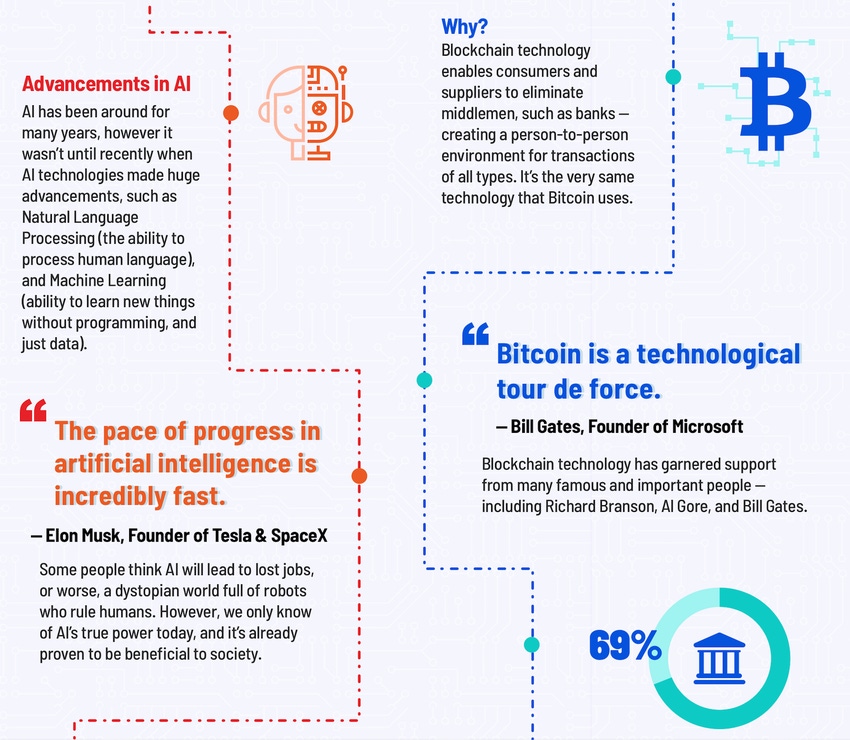

Infographic: AI meets blockchain

May 3, 2018

By Anand Akela

LOS ANGELES - AI provides the benefit of intuitive self-learning algorithms, many of which have been developing for years. Blockchain provides a decentralized infrastructure that is not controlled by any particular person.

AI has a lot of potential in the analysis of big data, enterprise, sales, and e-commerce data. One of the most common uses of AI in everyday life is bots on Amazon and Facebook looking at what you have purchased or viewed in the past to recommend similar products. The obvious problem with this behavioral data are privacy and security — it can be hacked (Experian) or misused (Cambridge Analytica).

This is where blockchain comes in. By providing a decentralized database, data can be stored in a safe manner, which can be interpreted, analyzed, encrypted, and stored on multiple devices — and even if you have some subset of servers failing or hacked, no one person can make sense of the partial data, only the decentralized AI algorithms can understand and analyze the data. AI is powered by data, and blockchain helps protect the data. Everyone should get excited about this.

AI has matured a lot, but blockchain is still its initial stages. The tools have evolved over a period of time, however there is lack of talent because the technology is so new. It’s important for people to start learning, and think about much bigger and disruptive ideas, such as a decentralized social network, but the user acquisition can be difficult from mainstream services. In 5 or 10 years from now, people are going to realize and take privacy seriously, giving these new services more traction.

Both AI and Blockchain are so powerful, so they can be misused if put into the wrong hands. With AI, once it is deployed you can’t always control it because it is self-learning, so in a way it is like a double-edged sword. Blockchain has similar issues, giving power to the people, for example through decentralized currency.

You May Also Like

.jpg?width=700&auto=webp&quality=80&disable=upscale)

.jpg?width=700&auto=webp&quality=80&disable=upscale)

.jpg?width=700&auto=webp&quality=80&disable=upscale)

.jpg?width=300&auto=webp&quality=80&disable=upscale)

.jpg?width=300&auto=webp&quality=80&disable=upscale)

.jpg?width=300&auto=webp&quality=80&disable=upscale)